When I Track Expenses and When I Don’t – The First Step to Budgeting

This website may earn commissions from purchases made through links in this post. As an Amazon Associate, I earn from qualifying purchases.

Tracking expenses has been great for helping me understand my spending. But life is too busy to do it all the time. Here’s when I find it most helpful.

I used to track every cent. For years. The Friday nights I’ve spent entering receipts into a spreadsheet….

But I’m no longer a fan of long-term expense tracking.

It’s time-consuming, and a little bit backward if you’re trying to save.

Because tracking expenses is like trying to train a horse after it’s already bolted.

But…

There are times when tracking expenses has been useful, so I’ve found it’s important to know when it’s worth doing.

That photo above? It’s not just pretty—it’s a metaphor. Tracking expenses involves following the trail of money that I’ve already spent.

I’ve found that a good budget helps me be proactive with my money, not reactive. Looking at my expenses after the fact and thinking, “Oops, we overspent,” hasn’t helped me much in terms of reaching financial goals.

That’s part of the reason why so many budgets fail (mine included, in the past).

So, what’s the purpose of tracking your expenses?

For me, it’s about understanding my current spending patterns and habits. Because saving money isn’t about spreadsheets or financial apps, but everyday habits.

They say that knowledge is power. And knowing where my money goes has given me the power to take more control of it.

It’s the foundation on which I’ve built a more proactive plan for managing money.

Disclaimer: This is general information only. In this blog, I share my savings and budget planning and what works for us, linking to authority websites where relevant. You should always consult a qualified financial expert when making money decisions to tailor plans to suit your circumstances.

When I Track Expenses and For How Long

So, when do I track expenses?

If I ever find myself thinking: “Where did all my money go? I could’ve sworn I had a fifty in my purse yesterday!” That’s usually my cue to check in with my spending.

If:

- I’m creating a budget for the first time

- My circumstances have changed

- I’ve become a bit complacent and want to spot the leaks and get back on track

…then it’s a good time to track expenses for a while.

While many financial experts recommend tracking every expense indefinitely, real-life experience shows that most people find this unsustainable. NAB research found 50% of Australians don’t regularly sit down to look at their finances.

And I get it.

There are multiple reasons why people don’t regularly track expenses, including time and effort, and information overload.

That’s why I prefer a more practical, habit-focused approach.

For me, the point is to understand my habits. Unless I’ve made a major lifestyle change or costs have skyrocketed (hello, inflation), I don’t feel the need to track for months on end.

Most experts wouldn’t agree with that – many recommend daily tracking. But I figure, if half the population doesn’t find that sustainable, it’s worth exploring alternatives.

(Although, if you love analysing data, then track your expenses for as long as you like).

Having said that, I do find short-term tracking super helpful. It gives me a good picture of what’s going on.

Even just a fortnight can be revealing.

But tracking for at least a month or two gives me the best insight into my patterns.

But tracking expenses isn’t my goal.

The real goal is adjusting my spending to support my long-term financial goals.

It’s just a data collection exercise—nothing more, nothing less.

Note: while I no longer track every single cent in a spreadsheet, I do keep an eye on my bank records to ensure nothing is amiss (i.e., fraudulent expenses are not happening), and I use a digital envelope system where I have allocated amounts of money for different categories. This makes it easier to keep spending in check without having to track every cent.

How I Track My Expenses

I first wrote about tracking expenses before smartphones were a thing and before there were hundreds of budgeting apps available to keep track of your expenses easily.

Now it’s much easier—apps make on-the-spot tracking super convenient. I’m not spending my Friday nights with a glass of wine and Excel anymore.

And if I use my bank’s expense tracker—or an app that links to my accounts—tracking becomes automated.

But here’s the thing: while automation makes it easier, I don’t think it necessarily makes it better.

Why?

Because when I rely on automation alone, I’m not actively engaging with or analysing my spending.

Automation helps with saving, but not so much with understanding my habits.

What’s worked best for me is combining approaches: using an app for ease, but also pulling out a spreadsheet—or even just pen and paper—to really get hands-on with the numbers and spending habits.

The Nitty-Gritty of How I Track Expenses

The devil is in the details, so here’s how I track expenses when I need to get control of our spending.

Step 1: I make a note every time I spend money. I might use my phone, a small notebook, this printable tracker, or save receipts to enter later (but not too much later—it becomes a chore fast).

Coffee? Write it down. Online purchase? Add it to the list. Quick supermarket run? Note it down.

I include what it was, which category it fits into, and the amount.

Step 2: I check for automatic payments—mortgage, insurance, subscriptions, charity donations, etc.—so nothing gets missed.

Step 3: If possible, I get the rest of the family involved. The more complete the data, the more accurate the picture.

That said, I’ve learned it’s not always realistic. Some people don’t want every purchase tracked, which is fair enough.

To keep things peaceful, I’ve sometimes just added a “partner’s expenses” line and guestimated.

Analyse Spending Patterns

Once I’ve got a month or two of data, I sit down to look for spending patterns and see where I might want to make changes.

Step 1: I sort everything into categories. Apps usually do this automatically, or I’ll manually label each entry if I’m using a spreadsheet.

Personally, I’m an Excel lover (former accountant habits die hard), but pen and paper works just as well—sometimes better!

Even with apps, I find it useful to download the data into a spreadsheet or print it. Trying to make sense of it on a tiny screen doesn’t give me the full picture.

Everyone will have different categories—what matters is choosing what makes sense for your situation.

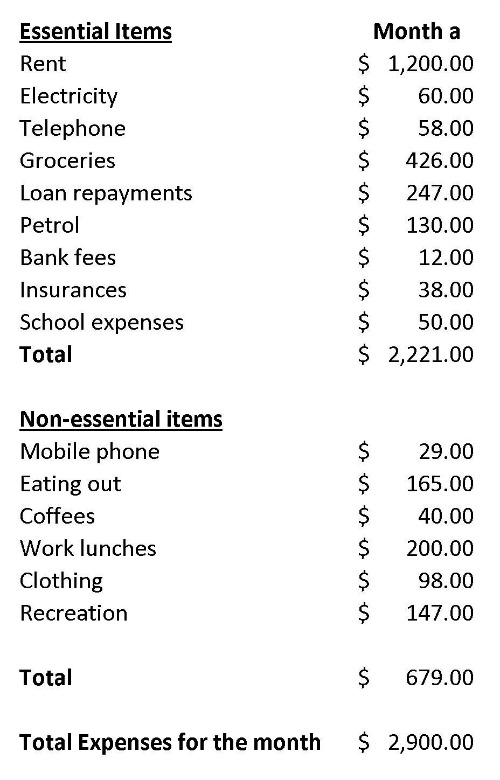

Here’s a basic example.

What I Do With the Tracking Info

It’s important for me to remember that this data isn’t a budget.

It’s just information. It tells me where my money has already gone. A budget is about planning where it will go.

Once I’ve got the data, I ask myself:

- Am I spending more or less than I earn?

- Are we saving anything?

- Did any numbers surprise me?

Even after decades of doing this, I still find little surprises.

Because small expenses add up, and it’s not until we track exactly by how much that we get a picture of the true impact of our spending patterns.

Like when I realised how much we spent on lunches. $12 here and there didn’t seem like much—until I added it up. That’s $240 a month. Nearly $3,000 a year.

That’s a holiday!

These little surprises help me see the opportunity cost. What could that money be doing instead?

Tracking forces me to think about habits I might not have noticed otherwise.

(Further Reading: Get into the Frugal Habit with a No-Spend Month)

Once I’ve got a handle on my spending, I usually stop tracking. No need to keep going—unless I want to.

What I Do Next (Hint: It’s Not Budgeting)

Wait—shouldn’t the next step be writing a budget?

Here’s what I’ve learned: writing down that I’ll only spend $50 a month on lunches isn’t enough. It sounds good, but if I haven’t created a workable alternative, I’ll just fall back into old habits.

Research backs this up. A 2018 study done by the University of Minnesota found that budgeting makes spending unpleasant, meaning people are less likely to stick to it.

So instead, I focus on changing the spending habits that led to the overspending in the first place.

That means prepping lunches, planning ahead, or making rules like “buy lunch only on Fridays.”

Once those habits are in place, the savings usually follow naturally.

Then, I can create a budget that fits our actual lifestyle—what we’re already doing—instead of wishful thinking.

That’s how I build a proactive money plan: one that manages itself, fits into daily life, and actually works.

Have you tracked your expenses? What did you learn? Any surprises? I’d love to hear your experience – drop a comment below.

Hi Melissa,

I had a laugh when I saw $60/month for electricity. Our last bill for 3 months was $650

My hubby was livid. We have changed plans.

It is so true that to succeeded one has to change habits, replacing the old with new. And ask how you are implementing the change.

thanks

Irene

I know, right! I made that table up a few years ago now and I haven’t had time to update it – goes to show how much electricity has gone up over the years!

Hi Melissa,

brilliant idea to develop habits rather than just writing a budget. I’m going to focus on some habits I’ve lost which were saving me lots of money.

Madeleine

Hi Madeline,

That’s awesome. Good luck :)

Mel