Snowball Your Savings

This website may earn commissions from purchases made through links in this post. As an Amazon Associate, I earn from qualifying purchases.

You’re busy saving for that holiday at the end of the year. But there’s also the emergency fund that needs boosting, you need to save for the car insurance, your Christmas fund, a house deposit…

How do you manage multiple savings goals?

I wrote previously about using excel to track your savings goals. This is a great method for monitoring your savings progress, but how do you divvy up the limited amount of cash that you have to put towards all these savings goals?

In order to manage multiple savings goals, we can borrow from the snowballing debt concept to streamline our cash. Here’s how it works.

1. Decide on your savings goals.

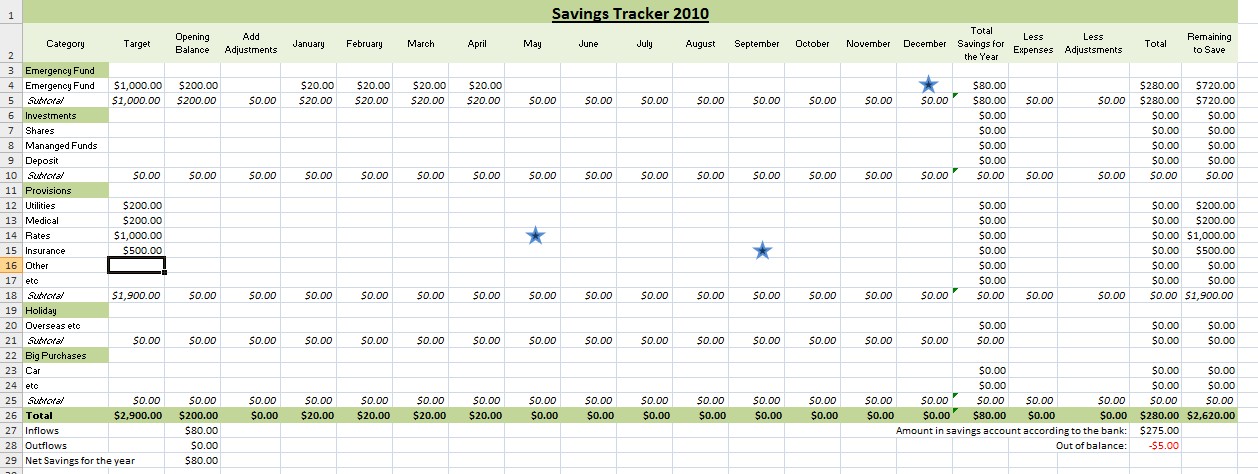

Decide on the things that you want to save for, holidays, big-ticket purchases, emergency fund, upcoming bills etc. Either write down your savings goals or use the excel savings tracker.

2. List your goals in either priority or by the due date or smallest to largest

If you’re like me, you have more savings goals than you do cash to put away each month. Prioritise your goals and save for those that are most important or imminent and then use the snowballing technique to save for the rest. If you’re using the savings tracker, I like to put a star on the month that things savings goals fall due.

3. Work out how much you need to put away each month

If your rates are due in six months and they are $1,200 then you know that you need to save at least $200 a month to reach your savings goal.

4. If you can, put extra toward the first savings priority

You may not have a whole heap of extra cash to throw at your savings goals. This is where snowflaking can boost your savings. A couple of dollars here and there will get you that little bit closer to your savings goal.

5. Initiate the snowball

Once you have reached your first savings goal, put the monthly amount that you had been saving towards that goal (plus any extra) towards the second goal, and so on.

A Hypothetical Example

| Priority | Goal | Time to save | Amount | Monthly Amount Needed | Actual Amount Cont. |

| 1 | Emergency Fund | 6 months | $2,000 | $330 | $400 |

| 2 | Washing Machine | 6 months | $1,500 | $250 | $180 |

| 3 | Holiday | 16 months | $6,000 | $375 | $100 |

- It will take 5 months to save up for the emergency fund.

- At the end of the 5 months, there will also be $900 saved towards the washing machine.

- In month 6 $580 will be put towards the washing machine (the usual $180 plus the $400 from saving goal 1), leaving $20 remaining. We haven’t quite reached our saving goal in the six months, but with only $20 to go we can either snowflake the $20 find it from somewhere in our budget, take it from our holiday savings or better yet, haggle on the washing machine.

- At the end of month 6 there will be $600 saved towards the holiday. In month 7 and following $680 can now be put towards our holiday savings. It will take another 8 months to save for the holiday, reaching $6,000 in 14 months.

- If, on the other hand, more savings goals arise, $540 will have to be put aside each month to reach the holiday savings goal within the 16 month time period, the remaining $140 to go to other savings goals.

In the past, I’ve been a bit haphazard as to which savings goal I am focusing on. I like the idea of being systematic because this way you know that you’re going to reach your savings goal on time and you can fully automate this process, setting and forgetting, enabling you to focus on other things.