How I Create a Super Simple Budget That’s Easy to Maintain

This website may earn commissions from purchases made through links in this post. As an Amazon Associate, I earn from qualifying purchases.

Budgeting doesn’t have to be complicated or take up a lot of your time. Here’s how I create a simple budget that is easy and helps us save.

Looking for a way to create a simple budget? In this article, I’m sharing the one that works for us.

You may have heard of the budgeting system called a zero-based budget (if you haven’t, I’ll describe it below.)

It was popularised by the American personal finance bloke Dave Ramsey.

In this article, I’m going to share a variation to the zero-based budget – one I find more effective for our situation.

It’s similar to the standard zero-based budget, but there are a few key differences that make it easier to manage.

Disclaimer: This is general information only. In this blog, I share my personal savings and budget stories and what works for us. You should always consult a qualified financial expert when making money decisions (not a random stranger on the internet like me – or even your mate at the pub).

But before I get into my system, let me briefly explain how the standard zero-based budget works.

The Standard Zero-Based Budget

In the standard zero-based budget, you create a budget every month by adding up all of your income and then adding up all of your expenses, savings, and debt repayments.

Then you deduct your expenses from your income. It’s zero-based because when you take your expenses/savings/repayments away from your income, your budget should equal zero.

Income – Savings – Debt Repayments – Expenses = 0

In other words, every cent of your income is allocated in your budget to either savings, living expenses, or debt repayments.

This type of budget is good in that you’re being proactive with your money and making every dollar count.

But it can be hard to stick to and a lot of work because…

The next step is to track all your expenses during the month to make sure you stick to your plan.

And then next month…?

You create another budget (again!?) and do it all over.

There had to be a better way…

I used to prepare an elaborate budget (because I used to be an accountant and still love spreadsheets) and then track my expenses to see if I stuck to my budget or not.

And I had a 100% FAIL rate.

That’s right! I failed to stick to my budget 100% of the time.

This is going to sound a bit dodgy, but I no longer think the problem was me. I believe the problem is how traditional budgets are built (at least, how I was taught when studying accounting).

The good news is I found a better way to budget that turned failure into saving success.

While the budget I use is similar to a zero-based budget, it varies in some critical ways. Here’s how the budgeting system I use is different:

- My budget is based on a pay cycle rather than a month.*

- I have a “Yes!” buffer in my budget, which I’ll explain below.

- I couple my budget with a modern envelope system so I don’t have to worry so much about big bills throwing the budget (except when the prices go up a lot!). This was a budgeting game changer.

- I use automation, so I don’t have to track every cent we spend.

How I Made a Simple Budget That Works

A budget is a plan for your pay. That means deciding how to spend your pay before you get it.

You can do this monthly (and if you get paid monthly, a monthly budget makes sense), but I find it’s easier to budget for a pay cycle.

(*We get paid fortnightly and monthly, so I budget some expenses fortnightly, like groceries, and some expenses monthly, and we cover all the expenses between us.)

Below I take you through the steps I use to create a budget. But I have a few useful tips that helped us before I begin…

Useful Data Before You Start a Budget

For a budget to be useful, it needs to be based on actual spending patterns.

After years of budgeting (including creating budgets for other businesses as part of my job), I’ve found wishful thinking doesn’t work. A budget needs to be based on reality.

So, if you’re not sure how much you spend, it’s easier to do an expense tracking exercise for a few weeks (you don’t have to do it forever) to get a handle on your REAL spending.

It can be an eye-opener just how much small expenses can add up!

Budgets are more accurate if they are based on actual spending patterns, even if the aim is to reduce spending.

Side Note

Budgets don’t save money; habits do.

For example, budgeting how much money you intend to spend (or not spend) on work lunches doesn’t mean much if you don’t get into the habit of taking your lunch to work.

So here’s what I’ve found to be the foundation of our budgeting success. Before changing our budget, we focus on adjusting habits, and when we see results from creating saving habits, we adjust our budget accordingly and save more.

Here’s what we do before creating a budget:

- Track expenses for a month and categorise expenses as explained in this article.

- Log into our bank and download a year’s worth of statements for our transaction accounts and credit cards. This helps us work out our income and budget for the bills etc.

- I start with a piece of paper, a pen, and a calculator. I get fancy with spreadsheets later, but a pen, paper and calculator are easy first up. There are also a bazillion budgeting apps you can use if you prefer.

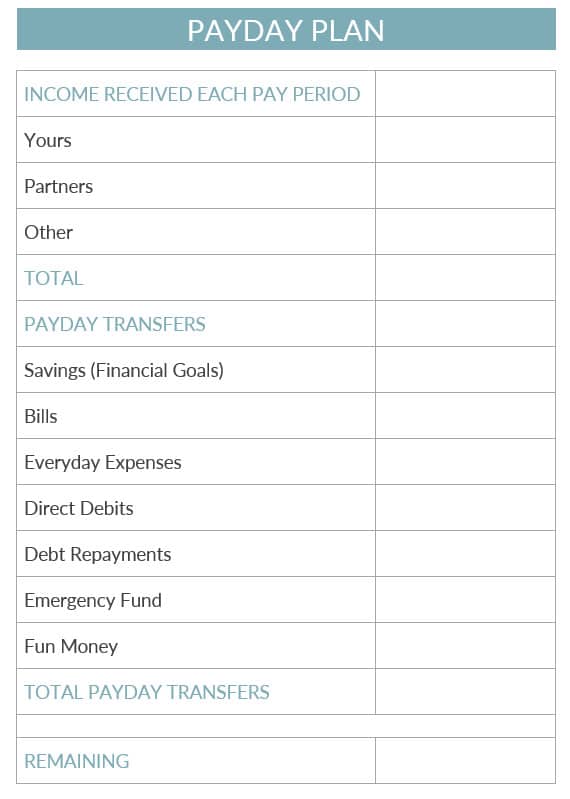

1. Write Down How Much We Get Paid Per Pay Period

The first step in creating a budget is to work out how much income “comes in” during a pay period. A budget would include my pay, my partner’s pay, and any other income we receive during a normal pay cycle.

As a freelancer, my income is not the same each month, so I budget for the minimum I am usually paid. If I earn more, the extra goes towards savings. The savings are there for any months I earn under what I expect, evening out my income. This is called income smoothing.

The next step is to calculate our “outgoing” money (expenses, savings and debt payments).

2. Start With Your Savings

The first rule of effective budgeting is to pay yourself first. So, the next step is to allocate some of our income to go to savings.

There have been times when money has been super tight for us. Sometimes all we’ve put aside is $2 per pay cycle. It doesn’t seem like much (it’s not, let’s be honest), but I’ve found establishing and maintaining the habit of saving is more important than the amount when you’re just getting started.

When we started reducing expenses, we already had a saving habit to build on. All we had to do was adjust our savings amount!

Creating a regular savings habit also allows you to establish and build an emergency fund, which makes life easier when unexpected expenses pop up.

3. Calculate Expenses

The next step is to write down expenses for the same pay period as the income.

Fixed Expenses

Some expenses will be easy (to write down, not necessarily to pay), like rent or mortgage, so it’s easier to start with these expenses first.

Subscriptions and regular direct deposits are all fixed expenses. We check our transaction statements to make sure we’ve covered all the expenses we would normally have in a pay period.

I try to adjust our payment dates to match our budget, but if I can’t, I either leave enough in a transaction account to cover them or treat them like irregular expenses below.

Discretionary and Variable Expenses

The tracking exercise for a month or so gives us a good idea of how much we spend on variable expenses, like groceries and petrol, and discretionary expenses, like entertainment.

From what we’ve tracked, we can write down a ballpark figure for these types of expenses. To start with, I’ve found it helpful to write down what we really spend, not what we hope to spend. Even overestimating is better because it gives us a little wiggle room.

Irregular Expenses

Finally, we come to irregular bills like the electricity bill, where we only pay them once every few months.

A big bill like this can really blow the budget, right?

It’s hard when you suddenly have to pay the rego or the electricity bill on top of all the regular expenses.

(And all our expenses seem to land in December, just before Christmas!)

This is where the modern envelope system comes in.

Instead of trying to find the money to pay for these bills when they arrive, it’s easier to plan for them in advance and stash away regular small amounts to cover them.

To do that, we use our budget (weekly/fortnightly/monthly) to allocate a regular portion of our pay to go towards the bills every payday.

For instance, we might put $20 aside every fortnight (or whatever the amount might be) to go towards the electricity bill, so when it comes in, we have enough to cover it.

Envelope Budgeting, Hacked

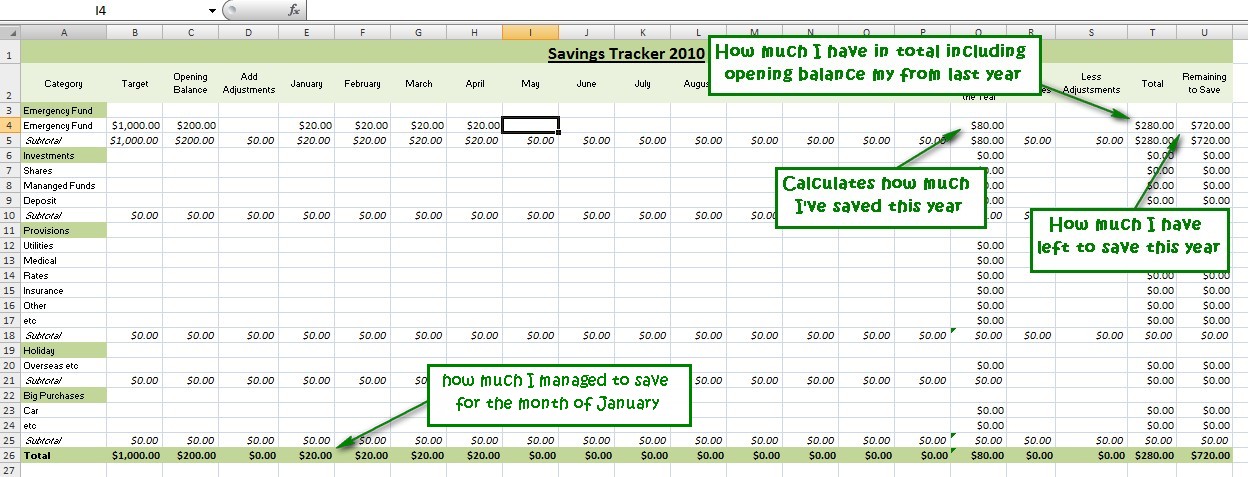

The above is the old envelope system, but instead of putting the money in an envelope, we put it in a bank account just for these expenses.

I like to track each amount in a spreadsheet, but it’s not essential.

You can also calculate once and just transfer a lump sum each payday without keeping track in a spreadsheet. If your bills are spread out throughout the year, you ‘should’ have enough to cover the next expense without having to cover all expenses at once.

This is how I track savings in a spreadsheet. I set it up years ago; it takes minutes a week to keep up to date. You can also use one of the many budgeting apps available.

When the bills come in, we’re paying them using the money already saved, not that fortnight’s pay. That fortnight’s pay gets allocated the same as every other fortnight.

It’s called BILL SMOOTHING, and it means that big bills don’t affect your budget (unless they go up a lot. Thanks inflation!).

It’s important to note that it can take a few months to transition from the old way of paying bills to the new way while you build your savings.

4. Debt Repayments

The last outgoing we budget for is debt repayments.

As with irregular bills, you can “smooth” these out by putting aside regular amounts each payday (in the case of direct deposit repayments) or just pay a regular amount each payday in the case of credit card repayments.

Again, this takes the highs and lows out of budgeting – your budget is pretty much the same each pay cycle.

5. Balance and Adjust The Budget and Add a “YES! Buffer”

The final step in our budget is we add up all our “outgoings” (expenses, savings and debt repayments) and write down the total.

Then take away this total amount from our income.

Income – Outgoings

We’re spending less than we earn if there is any money left over. Yay! If the expenses total more than the income, the budget will need adjusting.

As noted, the aim of a traditional zero-based budget is to get this income minus expenses amount to equal zero so that every cent is allocated.

But I like to leave a little leftover as a “YES!” buffer.

By that, I mean we have money left over to say:

“Yes! I can go out for a coffee today.” or

“Yes, kids, let’s have fish and chips on the beach this week!” or

“Yes, Amazon, I would like to read that book.” (A girl’s got to have one weakness!) or

“Yes! I will stock up on that staple while it’s half-price at the supermarket.”

(Sometimes, it just covers inflation.)

Sure, I could allocate this money, but the main benefit of the buffer is psychological, not financial.

If you feel that budgeting is boring, constricting, and takes away your freedom, a YES! Buffer gives some of that spontaneity back while still allowing you to save money and stay on top of the bills.

How much you allocate as a buffer is up to you and your circumstances, but even a couple of dollars a week can give you a little psychological wiggle room that gives life a little extra joy.

6. Automate Your Budget For Success

As I mentioned above, I don’t track expenses anymore – instead, I automate my budget.

(Sometimes, I do an expense tracking exercise for a month if we are in need of a budget reset or to adjust for inflation.)

I schedule payments each payday to go towards:

- Savings

- Emergency Fund

- Mortgage

- My “envelopes” for bills and other irregular expenses like Christmas and the dentist.

- Groceries and petrol

- our fun money allowance

Regular direct debits like Netflix come off our credit card. I have an automatic payment from my savings to my credit card for the same time of the month, so it automatically gets paid off straight away. I budget for these expenses as part of our bill-smoothing envelop system so the money is there to pay it. If we struggle, we cut the services and watch Vera reruns on iView (can’t overdo Vera).

My husband and I take a small “allowance” each for personal spending that we don’t have to account for. What’s left over (it’s often not much) is for our YES! Buffer.

It may seem weird, but this personal spending money gives us freedom while still contributing to the household kitty. It’s not much, but a bit of private spending money is important.

While it’s not practical to pay cash for everything, especially these days, it can certainly help us stick to a budget without having to track every cent because an empty wallet = no more spending.

As an alternative to cash, I use a prepaid debit card for my fun money that I can top up every payday. It’s sort of the same as cash in that once the money is gone, I can’t spend any more. And there’s an app to keep track of how much is left.

Because of rising costs, I need to check in with this automation every now and then and juggle the amounts (which usually means cutting back somewhere else).

Conclusion

So, that’s how we’ve been budgeting for the last few years. Of all the budgeting techniques I’ve tried (as an accountant, I learned and applied a lot of budgeting techniques), this has been the most successful for us.

What I like about it most is that it’s automated, so I can focus on what’s really important – good habits – and I don’t have to worry about the bills when they come in.

Do you keep a budget? How do you do it?

Thank you you so much for these valuable tips. I enjoy your articles. Really interesting.

Thanks T :). Glad to hear. All the best :)

Hi. This is my first read and I love it. I’m on a disability pension and I get that fortnightly. The way iv been doing things is a little different . But I will be trying with what you suggest as I can. Before I get my pension, Centrelink takes out my rent as I’m in a government house. I also arranged for them to take out some for each of electricity ,gas , and my phone. I always have a surplus with gas and electricity. Occasionally I get them to put anything up to $100.00 back into my account .this only takes 2-3 days. But I always make sure that money is left in there and that it won’t make me short when the next bill is due. My phone, because my needs have changed over time ,I havnt kept up with. It. So iv been working on that and will be in front again by the end of next month. I’ll stay that way. Now the first 5 months of the year my medication bill gets pretty high. Though I pay money off that each pay. Then when iv paid for as many scripts as the government requires, I catch up up again and then owe nothing to my pharmacy. I’m on my own and with my health the way it is I ever go out. So I have groceries, a monthly bill and birthdays and petrol money to the person that does all the things I need That is it. I’d like to know what you think. I never get to save anything. I knit for a charity so I asked on Facebook for wool and got a few people who gave me a lot of wool so oi don’t need to buy that. The one thing I need and so badly is steel interchangeable needles .now I only need about five but the cost is about $150.00 for a good set. Or small set as they say. That’s my goal. Sorry for all this info I’m giving you but I really would like your input Thankyou so much ?

Hi Wendy, thank you for sharing how you manage you finances. It sounds like your system is working well for you, I’m a big believer of don’t fix what isn’t broken.

I’m not sure what interchangeable steel needles are. I’m intrigued. Are they for knitting? You mentioned birthdays as part of your regular expenses, do you have a lot of birthdays you buy for? If so, maybe your friends and family who could get together to buy you those needles for your birthday??? What do you think?

using the budget to zero amount feels restricting and not enjoyable. I soo love the idea of a YES Buffer and having an envelope for all bills instead of seperate ones. Thankyou so much sharing, I will look forward to being able to buy that book I wanted with the YES Buffer this week :)

Hi Rhiannon, I hope you enjoy the book. :)

I love this!! I follow Dave Ramsey, but his method of budgeting is hard to implement and stick too. I am going to try this out and see how it goes. :-)

Hi Krista, I hope it goes well.

I have taken the envelope system one step further and actually, by using my banking system ,send the money to my regular bills each fortnight. Yes I know I am not getting any interest ,but I am not tempted to break into this money! I am actually now so far in credit with some bills I can actually reroute the payments to other things as needed or withhold the cash if necessary. It feels so good to get no RED Bills because I am always in the BLACK.The only annual bills I have to pay are the pink slip for the car and the green slip for rego, and the rego for the trailer.Everything else rates,electricity,insurance,telephone are already paid and I know any money in the bank is regular spendings or savings.

Hi Eileen,

Thanks, great tip. A lot of people have great success with prepaying bills like you do. It’s a great way to manage your money and interest rates are so low at the moment, it wouldn’t make much difference.

For people on Centrelink, they can choose Centerpay if they like to put money towards bills in the same way on their behalf.

Great ideas here, especially the ‘yes’ buffer. I hear you on the book purchases! Transitioning to the new system has an adjustment period as you said. If anyone is lucky enough to receive a tax return, back pay on family tax benefit or other unexpected cash this can be a great way to get up and running. Instead of spending the extra money put it straight to savings for upcoming bills.

I read somewhere that most people view unexpected money as a windfall to be spent, whereas others view it as an opportunity to improve their financial lives eg by investing it or implementing a better budgeting system like the one you’ve outlined.

Madeleine.x

Hi Madeleine,

Thanks for leaving a comment. Great idea about using a windfall to boost your savings during the adjustment period. It’s good to use a windfall to further your financial goals and it’s ok to treat yourself too :).

Hi Melissa,

Our income has always been low so budgeting and being frugal have been essential to my mental well being. I have been doing it for a few decades now and when I started out about 40 years ago I too used an envelope system but after all this time I am much better disciplined and don’t bother about envelopes anymore.

Now days I prepare a BUDGET spreadsheet every year with approx. 40 categories of spending with fortnightly and annual amounts. Then I prepared a second spreadsheet called ACTUALS with the same categories across the top and 52 lines for recording actual expenditure, one line for every week. Each row totals and each column totals with a row at the top of the column that shows remaining balances in each category and for the annual amount. I withdraw enough cash each fortnight for groceries, petrol and personal spending and leave the rest in the bank until it is needed. I pay most bills via BPay and have a credit card to pay bills such as mobile phone, internet, GoVia that have to be paid by direct debit. Under no circumstances will I ever enter into a direct debit arrangement with my debit card or savings account. When things go wrong (and they have) it is very hard to get a refund and it is also very hard to cancel direct debits. If things go wrong and the biller has my credit card account I can go to the bank and seek restitution for fraudulent transactions.

Sometimes stuff happens, the car breakes down, the dog gets sick etc and you have to pay bills that weren’t budgeted for. I therefore build in a contingency amount of around $1,500 p.a. and if we exceed that then I need to make adjustments elsewhere, for example no eating out for a couple of weeks or I delay going to the hairdresser for a couple of weeks.

When setting up the annual budget I also prepare a second “Dole Budget” which is a much reduced budget that allocates funds to the most essential of expenses as a worst case scenario should we both lose our jobs and have to go onto the dole. And it has happened. We did live for about a year on the dole before we retired and it was tough but we survived.

Our annual budget (expenses and contingency) is $34,000. We have no debt and because we are retired and living on our savings, I don’t factor in a specific amount for savings anymore.

Hi Colleen,

Thanks for sharing your budget! It’s very informative and I’m sure a lot of people will relate to your experience and find it helpful! Sounds like a great system that’s working well for you.

Thanks again. It’s lovely to hear from you.

Mel

Thankyou so much for the tips, it is really helpful. I’m a Registered nurse in my country and I’ve been finding it really hard to budget my income and yes this tips is really helpful.